Research

Planning for a Distributed Energy Future

Utilities are beginning to accommodate renewable energies, but many wonder if it is enough to keep up with consumer demand and prepare for new regulations

January 05, 2019

Much has changed in the past three years.

The rapid proliferation of DERs is the most obvious manifestation of the quickening evolution of the energy system away from the traditional hub-and-spoke model. Driven largely by state policy, financial incentives, and customer demand, this influx of solar, smart thermostats, EVs, battery storage, and other DERs is fundamentally reshaping the electricity industry.

- In the few short years since West Monroe’s last survey, Keeping the Lights On, there has been an increase in the types of DERs connected to the grid across utilities of all sizes and geographic locations in North America. In this research report, we take a comprehensive and linear look at how customers, utilities, and regulators are approaching this transformation.

What this survey demonstrates is that while the necessary actions and planning required by regulators and utilities to accommodate the wave of DER additions are beginning to take place, it is not at the pace required to be ahead of customer adoption rates.

Even so, the survey found that utilities are poised to rise to the challenge. More utilities now see DERs as an opportunity than three years ago, and many are making foundational investments to gain better visibility into their systems to understand what the tipping point might be for their business regarding DER penetration. No matter what the DER penetration is today, the next few years will be extremely important.

There are several likely reasons as to why DER planning by regulators and utilities is lagging that of broader customer adoption, including whether utilities are allowed to own generation or DERs, how much demand there is from customers, and public policy and regulatory factors in support of DERs.

In some cases, it may simply be a matter of DERs being spread out across an energy system in such a way that the impacts are either not yet noticeable or are focused on just a handful of circuits. For utilities and regulators, that leads to a logical question: If one or two circuits are most impacted by DERs, does it make sense to make systemwide investments?

Inaction has its own risks. One significant risk is that third parties could fill any voids where utilities aren’t meeting customer demand for DERs. By contrast, advanced planning by utilities and forward-thinking regulators can create an environment in which utilities, third parties and customers can all take advantage of the opportunities presented by DERs.

Introduction

Nearly three years ago, we took an in-depth look at how utilities, consumers, and regulators viewed the impact of the rapid proliferation of distributed energy resources (DERs) on the grid and utility operations.

The survey and subsequent report, Keeping the Lights On, revealed that while utilities and regulators understood that customer interest in solar, wind, energy storage, and electric vehicles was significant and rising, the actual adoption of DERs was still limited.

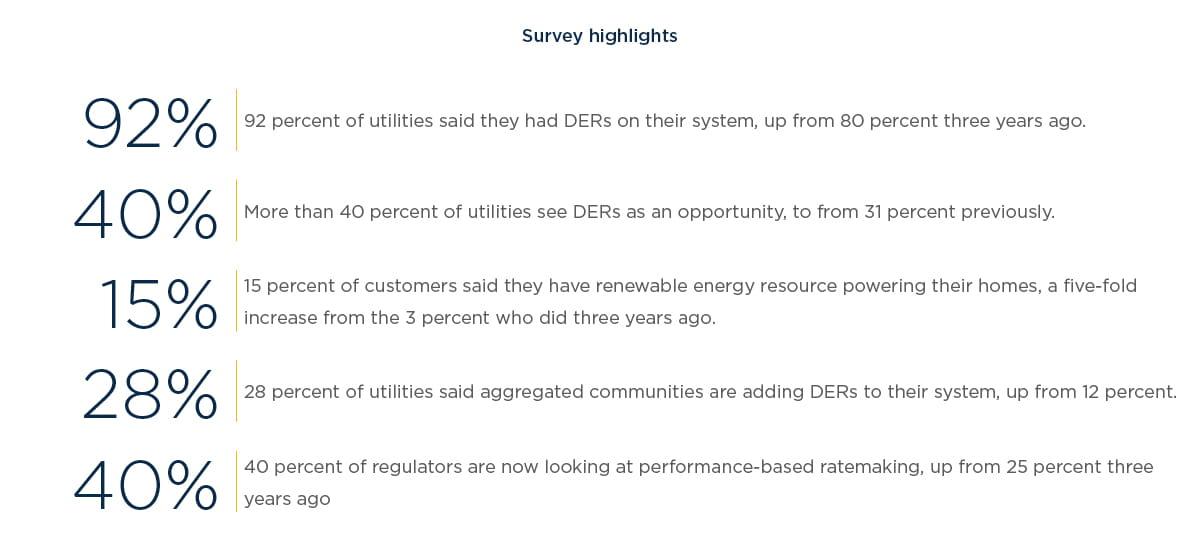

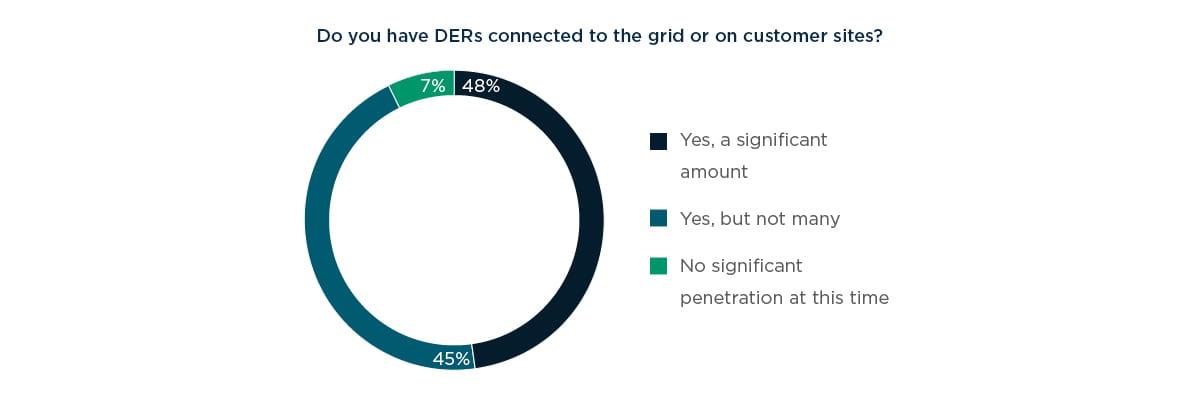

We recently returned to the market to follow up on how the distributed energy future is unfolding. This most recent survey, Planning for a Distributed Energy Future, reflects the continued deployment of DERs since the release of the last report: 92 percent of utility respondents now say they have DERs on their system, up from 80 percent in the last survey.

Overall, this survey found utilities are taking steps toward a decentralized energy future, but are not always proactively developing and investing in the services and digital systems needed to accommodate the increasing penetration of DERs. The failure to be proactive exposes utilities to risk. Given the multi-year planning efforts of utilities, many are hitting or approaching a tipping point where they will need a flexible, yet detailed, roadmap to guide the development of systems and processes necessary to accommodate and support DERs.

By not proactively developing the systems and processes needed to accommodate growing demand for DERs, utilities take the risk that large and small customers alike might completely bypass the utility grid in favor of self- generation, with or without utility backup service.

Chapter 1: DERs go mainstream, bringing uncertainty and change to utility operators

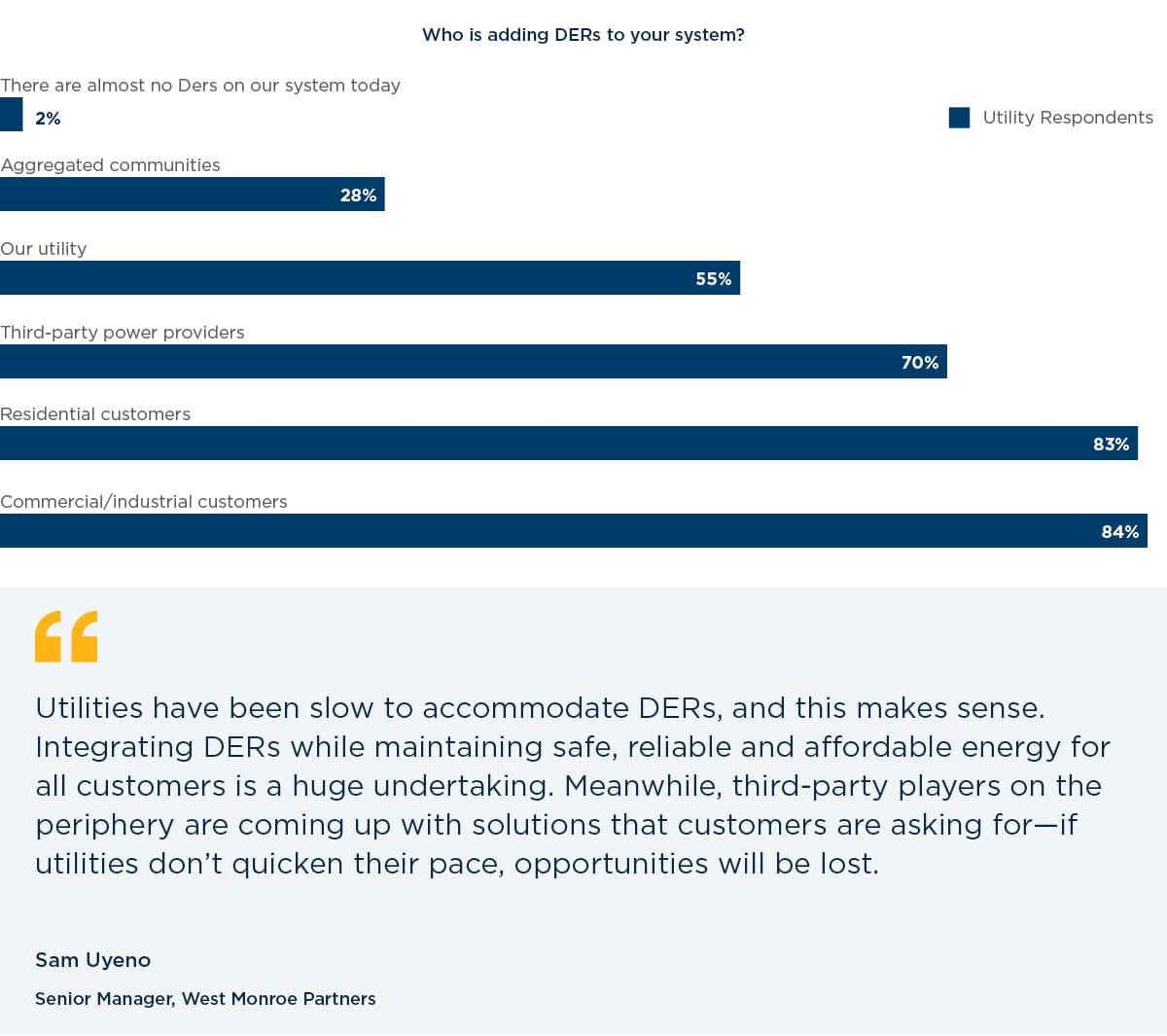

The survey data demonstrates just how much customer demand is growing. When utilities were asked about who is adding DERs, the answer is nearly everybody.

According to the Solar Energy Industries Association and GTM Research (now Wood Mackenzie Power & Renewables), the United States installed more than 32 gigawatts of solar PV in the past three years, thanks largely to the steep and ongoing decrease in the price of solar modules and inverters, as well as the extended federal Investment Tax Credit. Though the market has slowed somewhat in 2017 and 2018 compared to 2016, Wood Mackenzie Power & Renewables forecasts annual installations to return to more than 13 gigawatts annually in 2020 and beyond.

Besides solar, small-scale combined heat and power, smart thermostats, electric vehicles, and distributed energy storage have proliferated and are poised for even more future growth. In the case of storage, the total energy storage market in the United States is expected to double this year, and Bloomberg New Energy Finance projects that the global storage market will double six times by 2030 to 125 gigawatts. Forecast estimates for DER penetration consistently point to more and varied resources being added to the grid as alternatives to traditional utility distribution and transmission infrastructure investment.

While residential customers are still seen as driving most of the demand, 66 percent of utilities said third parties (other than customers) are adding DERs, up from 32 percent in the previous survey. Also, only 12 percent of utilities said aggregated communities were adding DERs previously, and that figure has now jumped to 28 percent. Utilities can work with third parties and aggregated communities to ensure DERs are deployed in a way that also support the grid, but depending on the regulatory construct, these entities may also be able to compete with the utility.

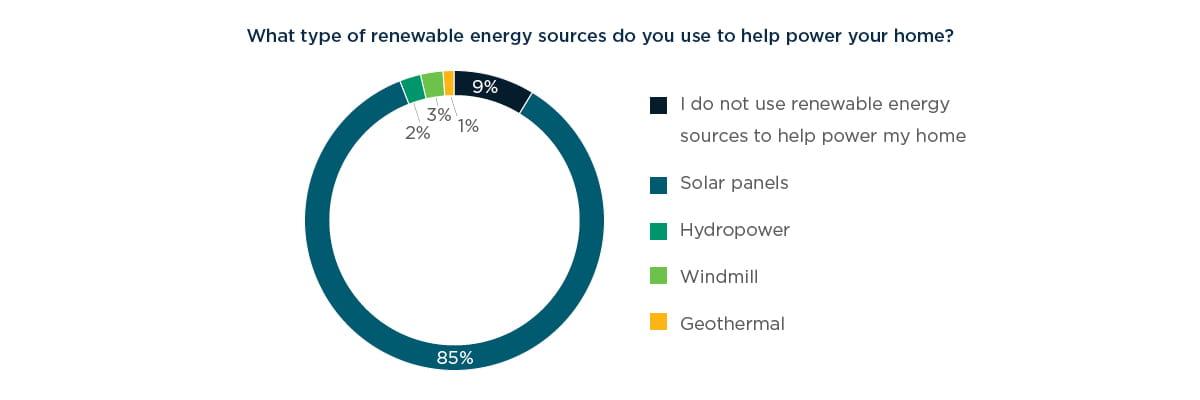

The growth is also seen on the customer side. Fifteen percent of customers surveyed said they have renewable energy resources providing electricity to their homes, compared to just 3 percent three years ago. For some of these customers, it might mean simply signing up to receive some or all of their electricity from wind power through their local utility, while for others it might mean investing in rooftop solar themselves. The majority of customers (60 percent) said solar is the renewable energy suppling power to their homes.

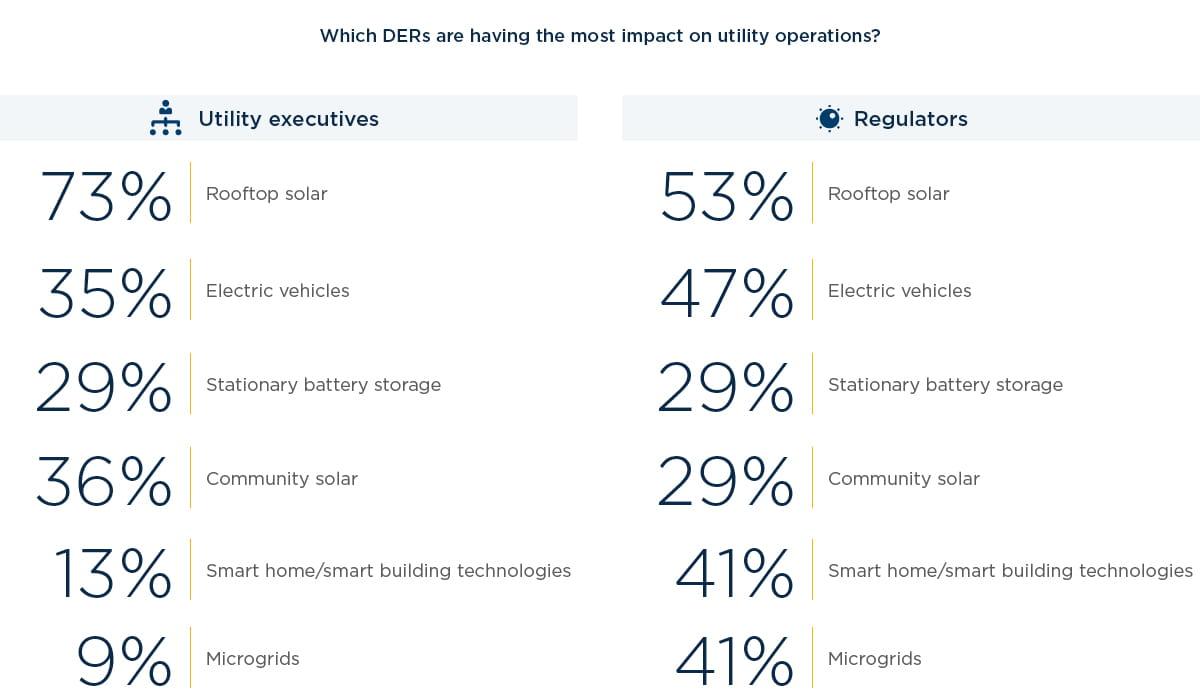

For utility executives, rooftop solar is still seen as having the largest impact on utility operations and loss of revenue. For regulators, however, the answers are more evenly weighted, with more than 40 percent of regulators noting that EVs, microgrids and smart building technologies will all impact utilities. That view on the part of regulators may encourage more technology-agnostic regulatory changes to accommodate DERs.

More than 90 percent of utilities said DERs are having some impact on their operations or revenue, yet nearly 60 percent said they had no specific management services available for DERs. This is similar to the figure three years ago, highlighting the mismatch between the proliferation of DERs connecting to the grid and the near-term utility planning necessary to accommodate them in novel ways.

“More and more utilities are experiencing DER proliferation, and the survey shows that. But the degree of DER proliferation varies by location, and their impact on utility systems isn’t well-known at varying penetration levels,” said Uyeno. “This uncertainty masks the potential risks of utilities and regulators not keeping pace with DER planning.”

Chapter 2: Coming to grips with DERs

For utilities and regulators, DERs represent a new way of viewing their businesses. Regulatory activities, such as New York’s Reforming the Energy Vision effort and a wide range of DER-supporting initiatives in California, might help explain why more utilities view DERs as an opportunity rather than a threat in 2018. Indeed, 41 percent of utility respondents viewed DERs as an opportunity, up from 31 percent in 2015.

“Thanks to improved grid technology, progressive regulatory frameworks, and successful DER demonstration projects across the U.S., an increasing number of utilities are beginning to view DERs as an opportunity as opposed to a threat,” said Uyeno. “We’re seeing much more collaboration among utilities, regulators and DER providers in crafting DER solutions that more closely align the interests of stakeholders and paving the way for future opportunities.”

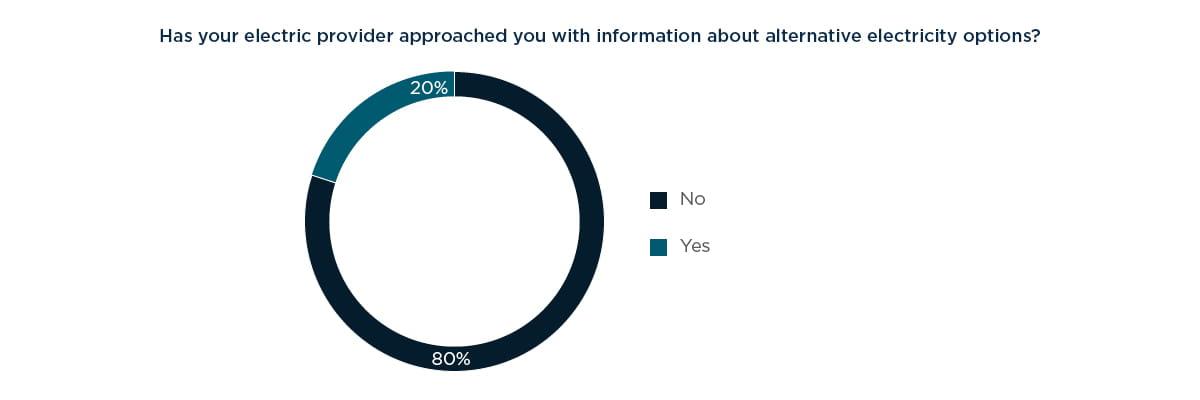

That said, 80 percent of customers report that their utility has not yet approached them with any alternative energy options, suggesting many utilities have not yet fully seized the opportunity or regulators have not given them direction or incentives to do so.

“In some regulatory jurisdictions, utilities are not allowed to own generation, thus non-utility providers or energy service companies are provided an opportunity to offer DERs directly to customers, so this finding is not surprising,” said Ross Kiddie, director with West Monroe.

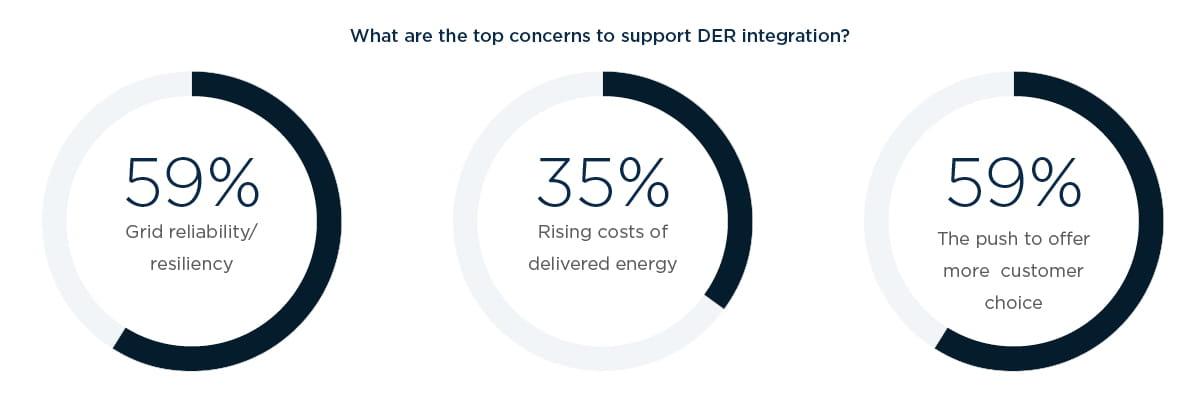

This year’s survey reveals that grid reliability is less of a concern for regulators than it was in the last report. Worries about rising costs are also receding somewhat, while the importance of offering customer choice is becoming a bigger priority to regulators. As a result, regulators are motivated to make or consider changes to support DERs.

“This finding is due in part to the fact that as more DERs have been added to the grid, no significant reliability issues have surfaced; this could likely be due to the fact that significant penetrations have not yet approached the tipping point at which such concerns might manifest,” said DeCotis.

Regulatory activity around the nation has supported pilot projects to show how DERs impact the grid, as well as to address the technical and financial challenges involved with incorporating more DERs. For instance, regulators in New York and other states are now requiring utilities to consider non-wires alternatives to traditional utility capital investments in transmission and distribution infrastructure.

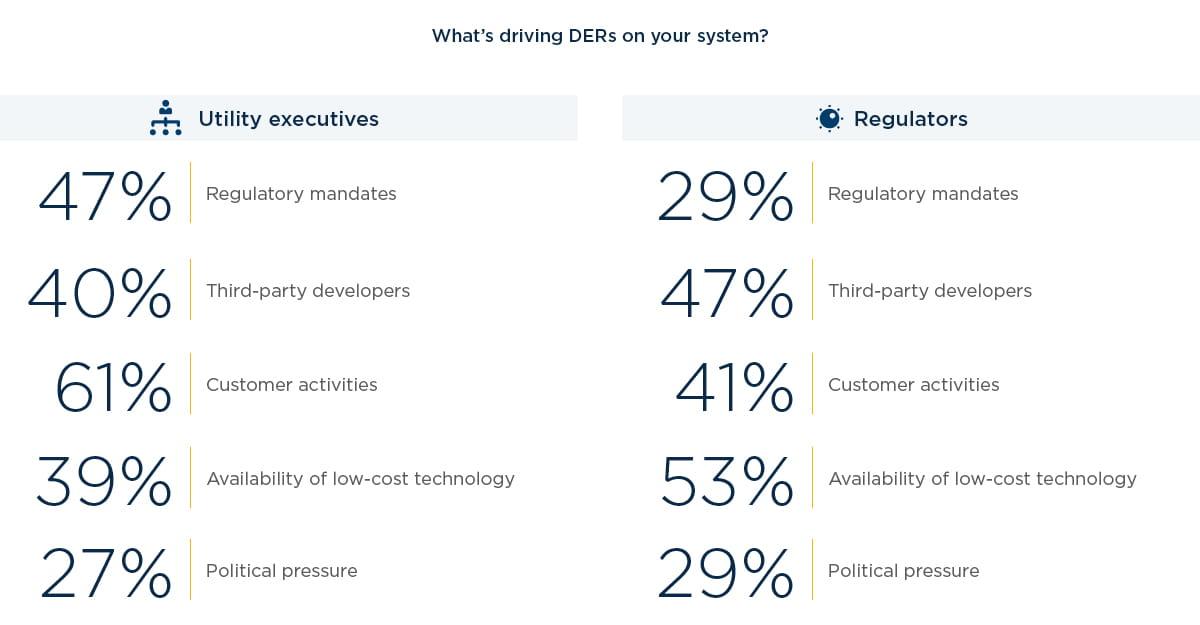

This is not to suggest there is complete alignment and agreement on the forces driving growth of DERs in different utility service areas. Utilities cite customer activities and regulatory mandates, such as renewable portfolio standards, as the primary forces driving increases in DERs. Regulators, on the other hand, pinpointed the availability of low-cost technology as the key driver. While perceptions differ, the increasing penetrations of DERs and their importance to grid operations are not always commonly understood.

Chapter 3: The moving target

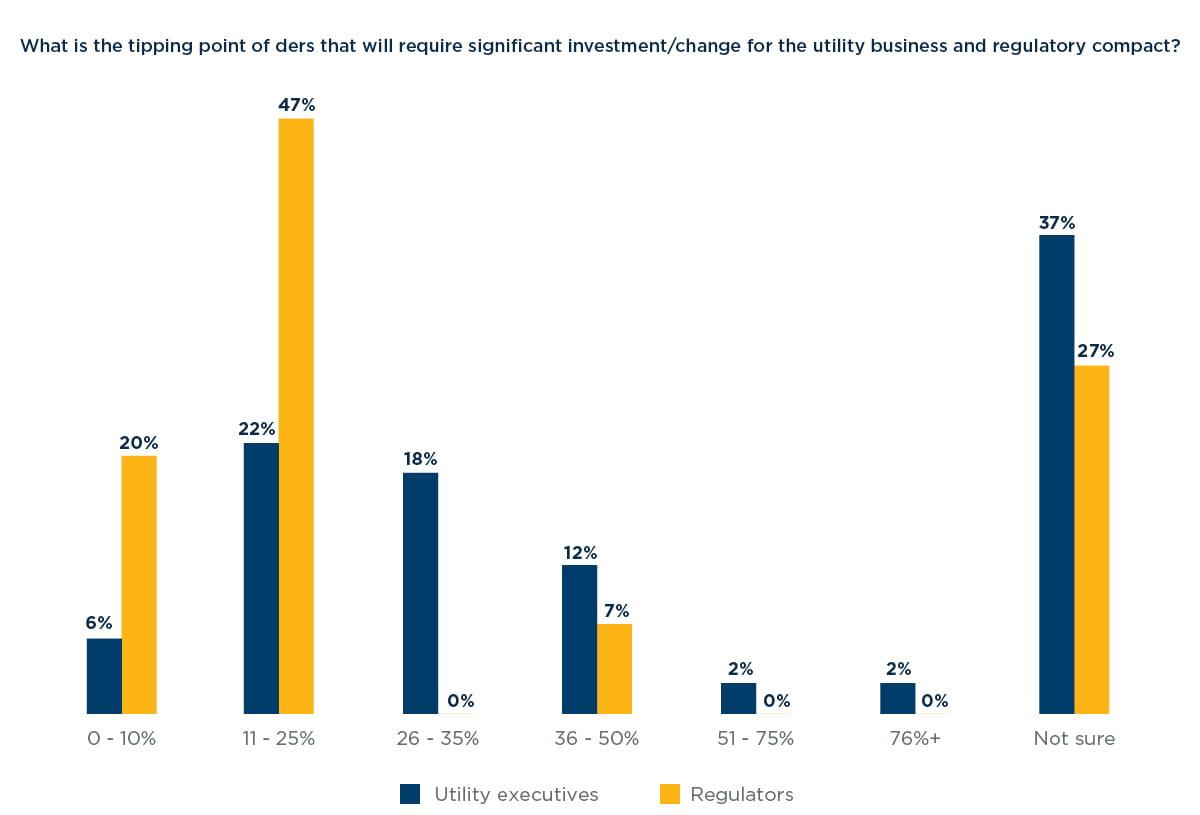

It has been difficult for regulators and utilities to clearly identify the tipping point of DER penetration that will necessitate significant investments to address potential reliability concerns. In most cases, it is a moving target depending on the current capabilities of the utility, current business processes and the prevailing regulatory framework.

In our last survey, nearly half of utility respondents said an 11 to 25 percent penetration of DERs would be the tipping point that would trigger those investments.

However, that perspective has changed markedly. This year’s survey shows that only about one-quarter of utilities (and almost half of all regulators) believe that penetration of between 11 percent and 25 percent will require big investments and raise the prospect of reliability problems.

This could mean that DERs are being sited and located on the grid in areas where such resources have the least negative impact or greatest benefit to the grid, or that penetration of DERs isn’t having the expected effects.

The change may simply be a matter of utilities having more experience with DERs or that DERs are being added to the grid where most needed, causing less of a concern for utility operations. As utilities make initial investments in systems to support DERs, they realize they are able to accommodate a higher penetration of DERs. Even utilities with low penetration are able to look to states such as California and Hawaii and benefit from their lessons learned.

While many utilities can leverage lessons learned from early adopters, each one will need a roadmap that includes investment plans for advanced business analytics and digital grid technologies, as well as business process changes and workforce adjustments to accommodate a new way of serving customers. Having visibility, and in certain instances, control over DERs on the grid to provide utilities with the tools needed to maintain reliability of their systems might also be necessary after penetration reaches a tipping point.

The increasing comfort level with DERs is encouraging, but also poses the risk of complacency. Without the right digital systems and visibility, many utilities will have trouble developing the necessary advanced analytics to identify when and where new investments are needed.

While initial investments such as advanced metering can provide data streams that may provide an additional level of insight, that is just the beginning. Increasingly, utilities need detailed, feeder-level data to inform where investments need to be made as more DERs come on the system.

Over one-third of utility respondents said they were unsure what the tipping point is for DERs on their grid. A precise understanding of what that tipping point is matters because it is so necessary for utility planning, which generally has an extended time horizon.

Obtaining that visibility can allow utilities to provide faster interconnection and more information to third parties and customers, and also create incentives for DERs to be placed on feeders where they would be most beneficial to the grid.

Chapter 4: A new way of doing business

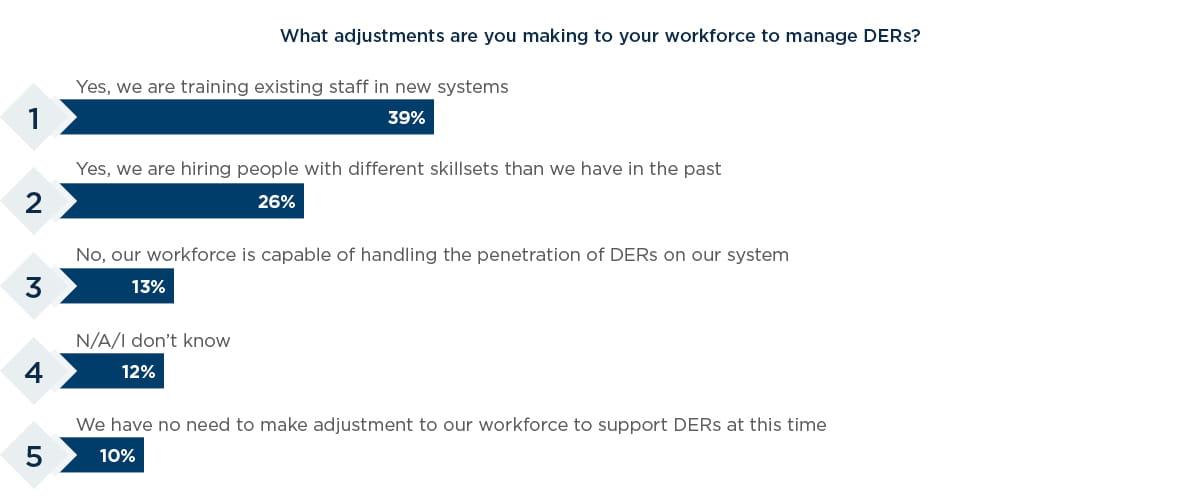

It is well-understood that many utilities face challenges as their workforce ages. But DERs also add another layer of complexity as utilities assess their workforce of the future.

For the first time, we asked utilities about hiring practices. Unsurprisingly, more than a quarter said they are bringing in employees with different skillsets than in the past, and nearly 40 percent said they are retraining existing staff with new systems. As the penetration of new digital systems proliferate, that number should rise even further in the coming years.

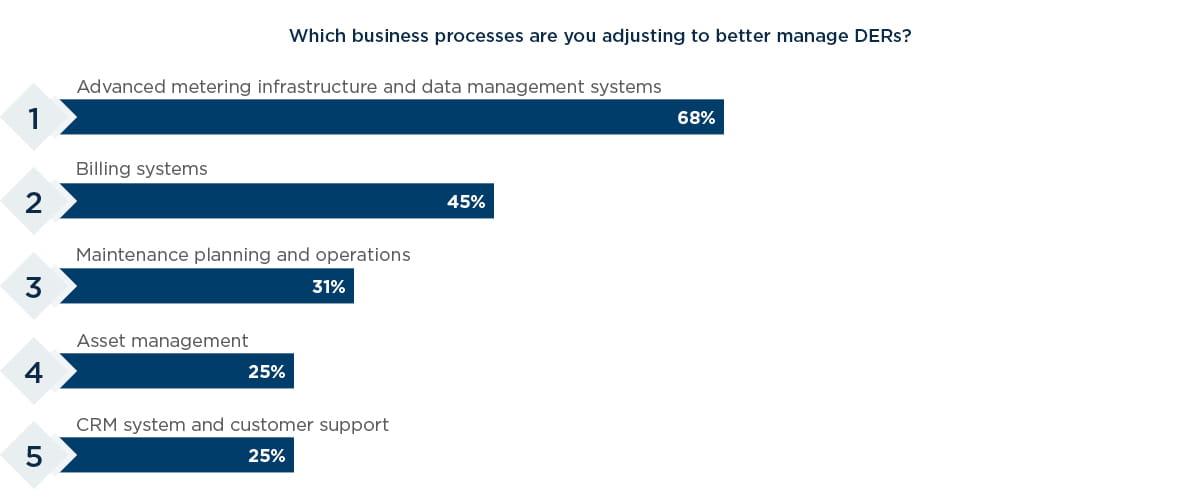

As for which systems are being updated, utility respondents noted investments in advanced metering technology and interconnection systems to better plan for more DERs. While foundational to plan for and accommodate more DERs, billing and advanced metering infrastructure are by no means sufficient by themselves.

The number of utilities investing in asset management and customer management systems, which are both important tools to plan for increased levels of DERs, actually dropped in comparison to the survey three years ago. That could imply that some utilities have completed those projects, but for others, it may mean there is more investment needed.

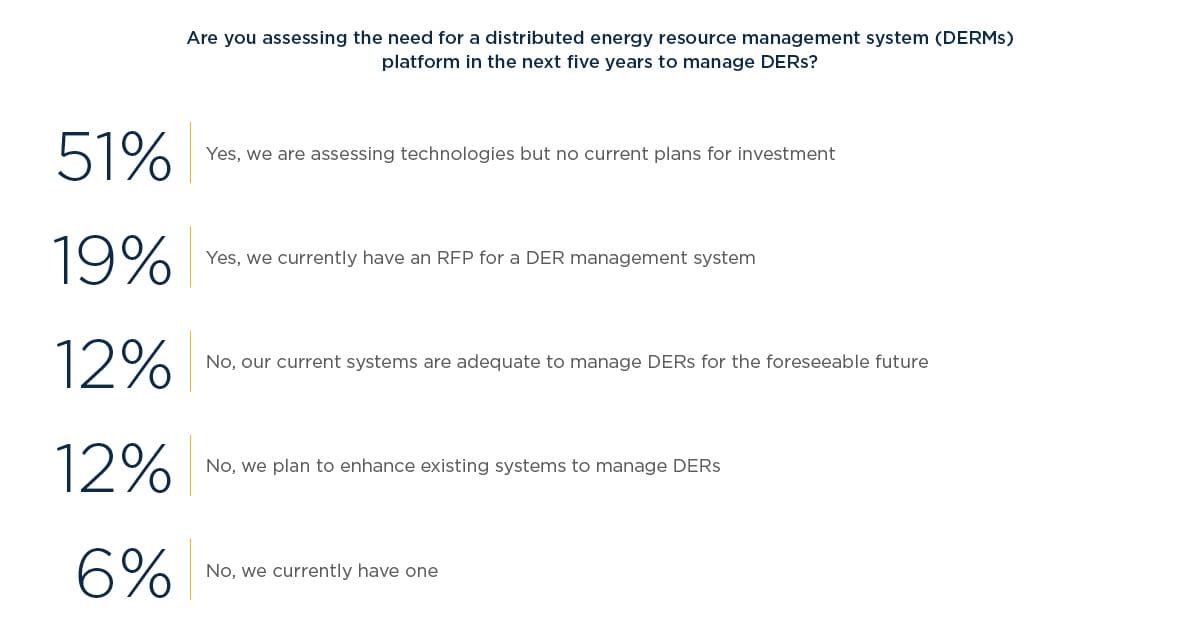

In a new question, we asked specifically about distributed energy resource management systems. While DERMS technology is on the radar of many utilities, half of utility respondents were assessing it without any concrete plans for investments. For many, they could be leveraging existing systems, such as an advanced distribution management system, or waiting for higher penetrations to necessitate the investment.

“Until we reach a tipping point where DERs are of significant scale that they threaten the utility’s ability to respond to outages or changes in load, we won’t see a lot of DERMS. In fact, if penetrations become too large in number and size, utilities might need to start looking at ways to control DERs on the grid to maintain reliability,” said DeCotis.

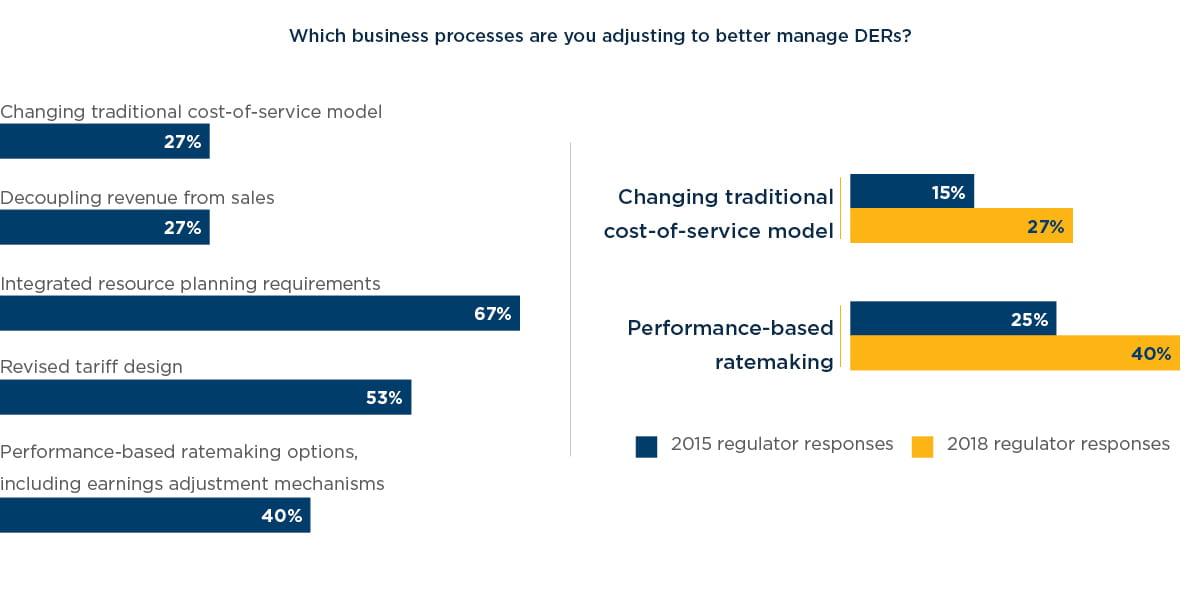

It’s not just utilities that need to ramp up their preparation and investments for more DERs. Like utilities, regulators in our survey are making changes to their traditional modes of operation. That is coming primarily in changes to the traditional cost-of-service model, as well as integrated resource plans.

The traditional relationship between regulators and utilities needs to evolve in response to DERs. Since the majority of utilities plan to recoup the investments required to handle greater amounts of DERs through traditional ratemaking, there is a need to align the scope of that investment with new regulatory designs.

Several states are also considering incentive or performance- based ratemaking to reward utilities for embracing DERs, including EVs, to increase options available to customers to meet demand, and for utilities to expand their resource supplies to meet demand, or grow load in the case of EVs.

One way that is already happening is through increased education about and activity around performance-based ratemaking. The National Association of Regulatory Utility Commissioners has hosted sessions to educate commissioners about performance-based ratemaking, and utilities that have piloted the approach have shared what they’ve learned. New York, California, and other leading states are already offering utilities the opportunity to recover investments and earn returns based on performance.

Our survey reflects that interest: 40 percent of regulators are now looking at performance-based ratemaking, an increase of 15 percent from 2015. The number of regulators now looking at changing the traditional cost-of-service model has almost doubled, from 15 percent in 2015 to 27 percent this year.

“I can see why there has been this general shift,” South said. “Some of the initial deficiencies of performance-based ratemaking have been revised through experience, and that has made it more appealing to other regulators.”

“The traditional cost-of-service regulatory model is really no longer applicable across all investments,” added DeCotis. He expects to see a hybrid model in the next three to five years in forward-looking states, with others following suit as regulators and utilities grow more comfortable moving away from the cost-of-service model.

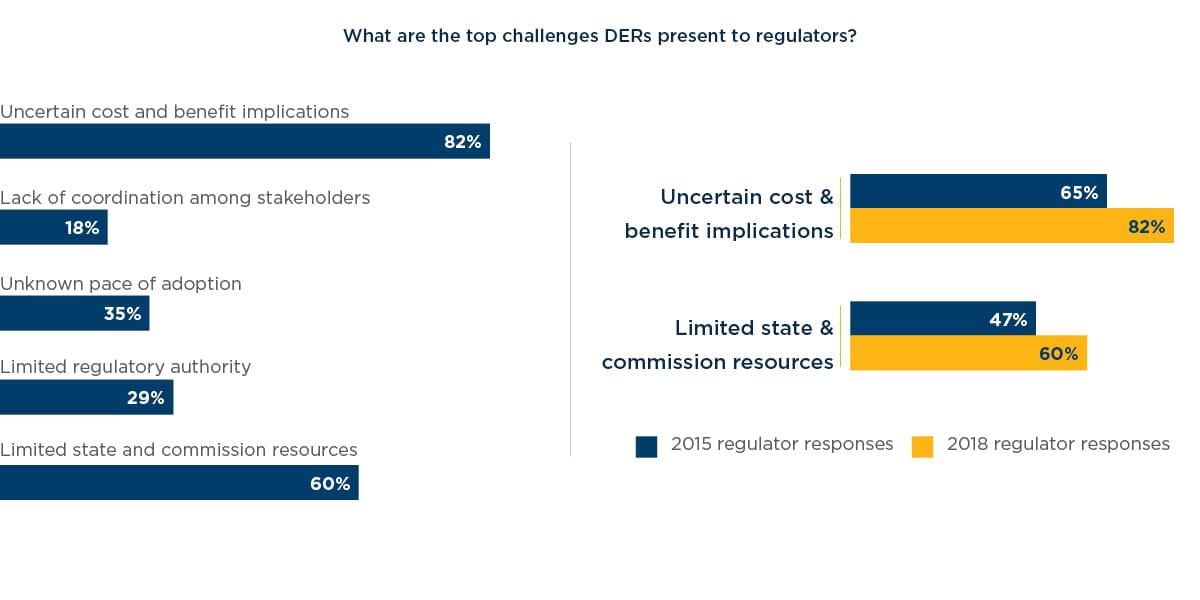

Traditional investments, replacing in-kind equipment or to maintain the backbone of the grid, might still be recovered through cost-of-service rates, and new, more innovative investments supporting a more dynamic distributed grid might well be recovered through performance-based rates.Additional education and investments to support the work of regulators are needed. The proportion of respondents who said there were limited state and commission resources to plan for the challenges of DERs increased from 47 percent three years ago to 60 percent this year, which indicates that more regulators are acknowledging that the scope of work needed to plan for DERs is beyond their internal capacity.

While customer demand and advances in distributed energy technologies are driving the increasing deployment of DERs, the expectations facing utilities and regulators for interconnection, financial and technical support, and reliability are more top-of-mind than ever before. Customers are more engaged, agile, and savvy, and they expect so much more from their local utility.

Conclusion

Though important, it’s not just a matter of satisfying customer demand. Planning to accommodate larger amounts of DERs provides utilities with new opportunities to increase customer satisfaction, enhance revenue and investigate new business models as ways to adapt to changing customer needs. The flip side is that failure to respond to changing customer demands and higher expectations can expose utilities in states where retail competition is available and third-party providers are offering DER services to fierce competition for utility and perhaps other non-utility services.

“Five years is now an eternity in the utility industry. Proactively planning for and investing in the digital systems, the workforce of the future, and business processes required to accommodate a large amount of new DERs is an imperative. Only by keeping up with or staying ahead of DER penetration, can utilities, regulators, and customers reap the full range of benefits available through a more distributed energy system,” said DeCotis.

Survey methodology

West Monroe conducted an online survey with responses from more than 1,700 customers, 140 utility executives and managers, and more than two dozen regulators in major markets across North America. The goal of this research was to revisit customer attitudes toward DER adoption, the ongoing impacts DERs are having on utility operations in the United States, and what both utilities and regulatory bodies are doing (or plan to do) to accommodate increasing customer demand for DERs from strategy through process and technology needs and system integration.