The rise of distributed energy resources (DERs) is an exciting and interesting opportunity for customers, and a challenge and opportunity for the utilities and the organizations that regulate them. DERs is a category of solutions that is inclusive of distributed generation sources like combined heat power (CHP), solar, and wind, as well as energy storage such as batteries. In this white paper, West Monroe takes a comprehensive look at how consumers, utilities and regulators are approaching – or resisting – this energy evolution. This research examines the present and future state of DERs through multiple lenses: customer adoption and awareness; utilities’ adoption challenges and opportunities, and support and planning initiatives; and regulatory commissions’ actions, obstacles and perceptions.

We found that while the presence of DERs among residential, commercial and industrial sites is still limited, customer interest is increasing and adoption is on the brink of booming in many states across the U.S. And though utilities and regulators alike acknowledge this potential shift, in many states they have yet to settle on clear and collaborative ways to prepare for it. Factors from technology availability and cost, to public policy drivers, to pivoting business models, are contributing to the obstacles slowing DER penetration across the U.S. These issues continue to impede the industry’s ability to smoothly accommodate new energy technologies and gain acceptance. By illuminating the gaps between customer needs, utility plans and regulators’ perceptions, it is evident that these audiences must form a more united front before meaningful change can truly occur in their state.

Introduction

The electric utility industry is accelerating toward a crossroads. Cost-averse and environmentally conscious customers are reducing their dependence on traditional utility generation and creating increased demand for distributed energy resources (DERs). If the market’s recent growth is any indication, DERs will become a more important part of the generation portfolio mix in the future.

Between the U.S. federal government’s enactment of the Investment Tax Credit (ITC) almost a decade ago and launch of the SunShot Initiative in 2011, the cost of solar energy installations has plummeted more than 73 percent. This trend is aided by the U.S. Department of Energy’s decision to double down on its support for renewable energy research and development and materials manufacturing. While technology costs continue to decline and efficiencies rise, rest-of-system costs are coming down as well, making photovoltaic (PV) solar more affordable. Federal support, along with utility and state-sponsored financial incentives for purchases and leasing of rooftop solar PV systems, has accelerated adoption of DERs by residential, commercial, and institutional customers.

In the last few years, the barriers to DER adoption have decreased significantly in many areas in the US. Solar generation is competitive with retail electricity prices in many parts of the country, and comparable to avoided transmission and distribution system upgrades in some utility jurisdictions. Cost reductions in DER implementation and interest in such systems apply across rooftop, utility- scale, and recently in community solar installations, providing opportunities for broad business and customer adoption. In 2014, a new solar project was installed every two-and-a-half minutes in the U.S.

As business and residential customers continue to seek more economical and sustainable energy solutions and utilities require cleaner energy power solutions to satisfy various regulatory requirements, distributed energy adoption does not appear to be slowing down anytime soon. General Electric predicts that annual distributed energy capacity additions will grow from 142 gigawatts (GW) worldwide in 2012 to 200 GW in 2020, an annual growth rate of more than four percent. Though this shift carries benefits for customers and the environment, it is forcing the utility industry and regulators to rethink the traditional utility business model and the sanctity of the utility franchise. As electricity generation becomes more decentralized and located closer to load, utilities are beginning to identify ways to maintain revenue and provide greater value to customers through alternative rate design, new utility business solutions, and creation of unregulated business enterprises.

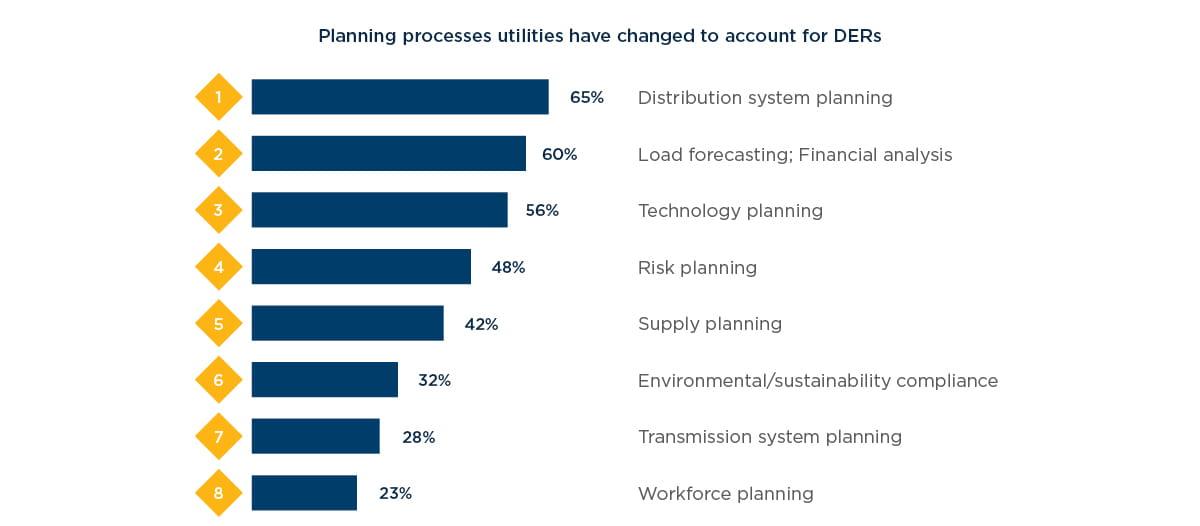

Chapter 1: The impact of DERs

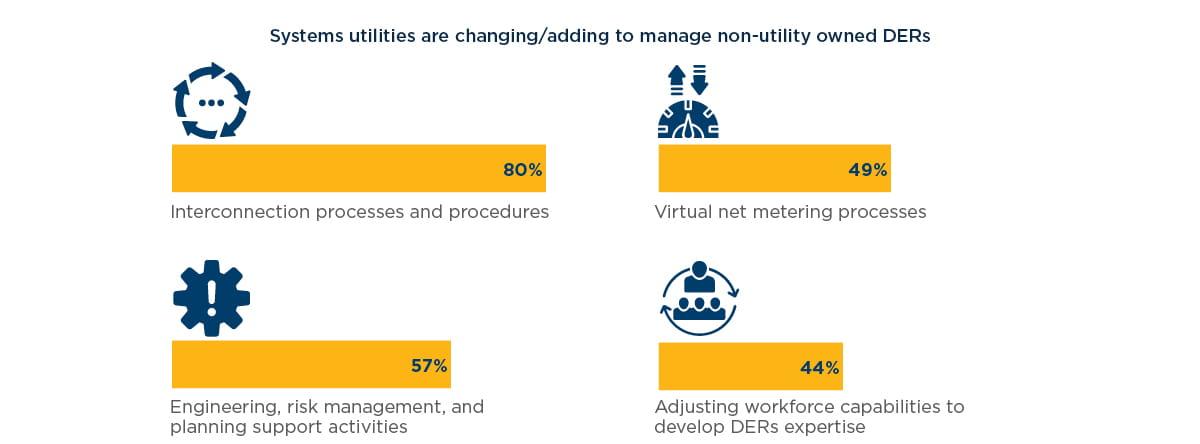

Distributed energy resources present a new layer of complexity to utilities’ operations, while at the same time promising to inject new life into the traditional business model. Eighty percent of utilities in our survey reporting have DERs on their systems, but executives and regulators do not share a common vision when it comes to how regulations currently (or should) impact DER support and ownership. Today, three percent of customers have renewable energy sources serving their homes, and 48 percent are considering doing so in the next two years. Only one percent of customers are enrolled in distributed generation programs through their local utility. The rapid rise of DERs on utility systems is also creating difficulties for utilities to enroll customers and manage the interconnection process. Many utilities and regulatory commissions are looking at electronic enrollment and interconnection software to improve customer engagement and satisfaction.

Seventy-nine percent of regulators feel that the current regulatory model allows and encourages utility ownership of DERs, compared to just over half (53%) of utility executives. This indicates a discrepancy between what utilities think they need in order to encourage and support DER ownership and implementation, and what regulators think utilities need. In certain markets, regulatory commissions think the regulatory paradigm supports DER deployment; however, they might lack the resources necessary to thoroughly investigate the regulatory changes needed to support utility investment and ownership.

Despite the number of utilities that report having DERs on their systems, only 37 percent offer DER-specific support services, systems or technologies. In the same way that smart grids have enabled utilities to transform how they distribute and bill for electricity, DERs open the door for utilities to capitalize on new business opportunities, including backup generation, load balancing capabilities, differentiated pricing regimes, and solar marketplace services such as vendor identification, financing, and maintenance. Many utilities, however feel the cost of creating these services outweighs the returns: 59 percent of executives say their utility plans to make no or minimal investments to support DERs on their systems unless mandated by regulators.

Early reactions to the rise of DERs

The majority of utility executives harbor mixed feelings about how DERs will affect their business. Regardless of how executives feel, an uptick in adoption is inevitable. Two-thirds (66%) of executives feel DERs are both a threat and opportunity for their businesses, three percent feel they are only a threat, and nearly a third (31%) feel they present an opportunity. Understandably, many executives seem confused or feel it is too early to claim that DERs will or will not wreak havoc on their operations. As discussed later in this report, executives’ actions reveal that most utilities treat DERs primarily as a threat.

Today, more than two-thirds (69%) of customers do not know if their utilities offer distributed generation enrollment, and 94 percent say their providers haven’t approached them about alternative energy options. This can lead to uncertainty and confusion about customer-sited DERs. As DER adoption grows, more customers will demand specific accommodations such as efficient distributed generation (DG) enrollment processes and management, and accessible DER diagnostics. Utilities that fail to provide a sufficient DER customer experience may suffer business and compliance consequences, and as a result, more oversight from regulators. Certain regulatory authorities (including the New York State Public Service Commission) are starting to require utilities to offer electronic DER enrollment to decrease customer effort and increase transparency around the DER interconnection process.

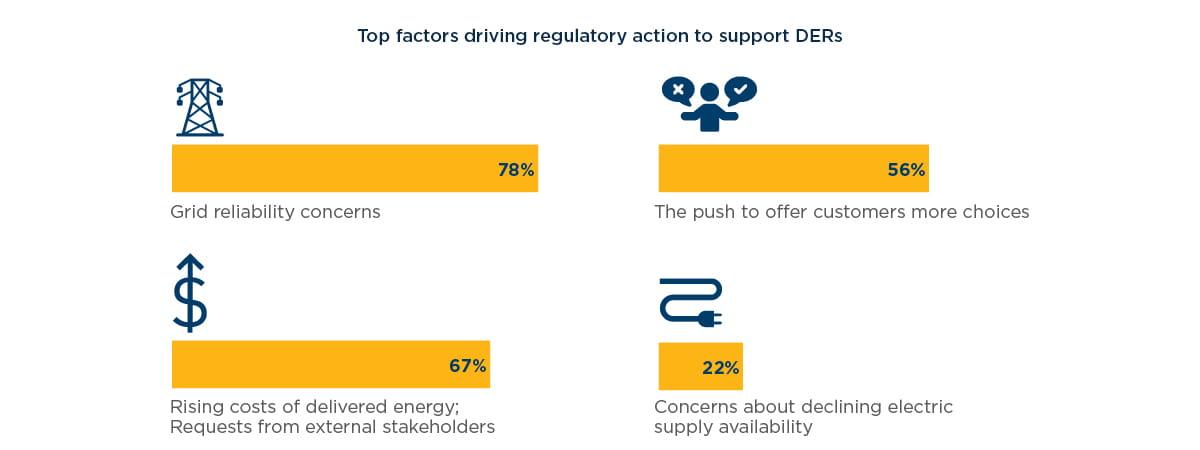

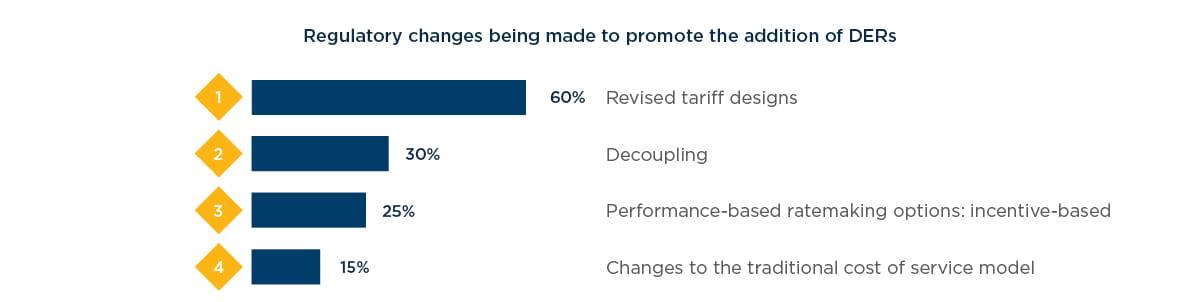

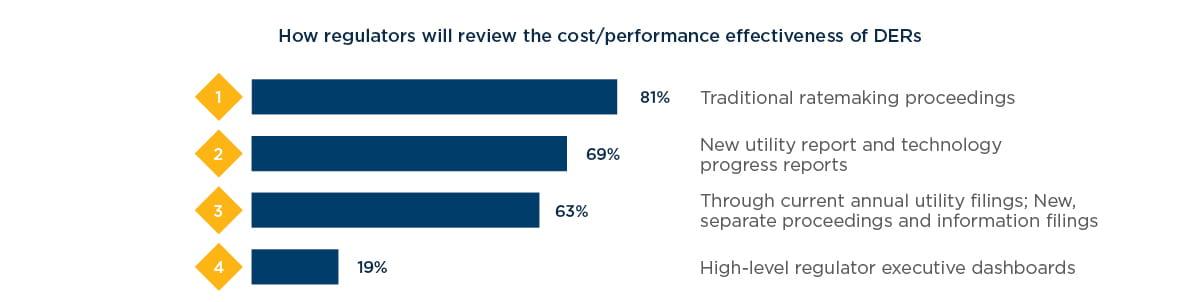

Regulators are already modifying their requirements and compliance paradigm to support DER integration. Regulators cited a handful of concerns driving the proposed changes: