Article

Why a digital operating model is necessary for banks to reach their goals

Lay the foundation for success in the digital age

April 29, 2022

Article

Lay the foundation for success in the digital age

April 29, 2022

With the ever-quickening pace of digital across the industry, banks are also now confronting an increasingly fragmented industry, splintered by new banks and big tech challengers creeping into the territory of traditional banks. Big Tech and fintech have revealed digital capabilities long thought impossible for banks to achieve on their own—and brought with them an acceleration toward open banking models across the industry.

Underpinning all of this is a new profile of today’s bank customer and the generational sea change and wealth transfer from Baby Boomers to the now dominant Millennials, who interact with financial services with very different expectations and needs.

On the inside, the profile of a bank employee is also evolving. As banks begin to look increasingly like technology companies in order to keep pace and compete with competitors, banks will also need to rethink their talent needs and prioritize digital-forward talent like technologists, data engineers, and non-traditional hires.

An often-underestimated tool for banks to leverage in their digital journey? Moving to a truly digital banking operating model. In our view, a digital operating model succeeds by keeping the client at the center of everything the bank does by creating capacity to focus and invest in those clients, when they need it.

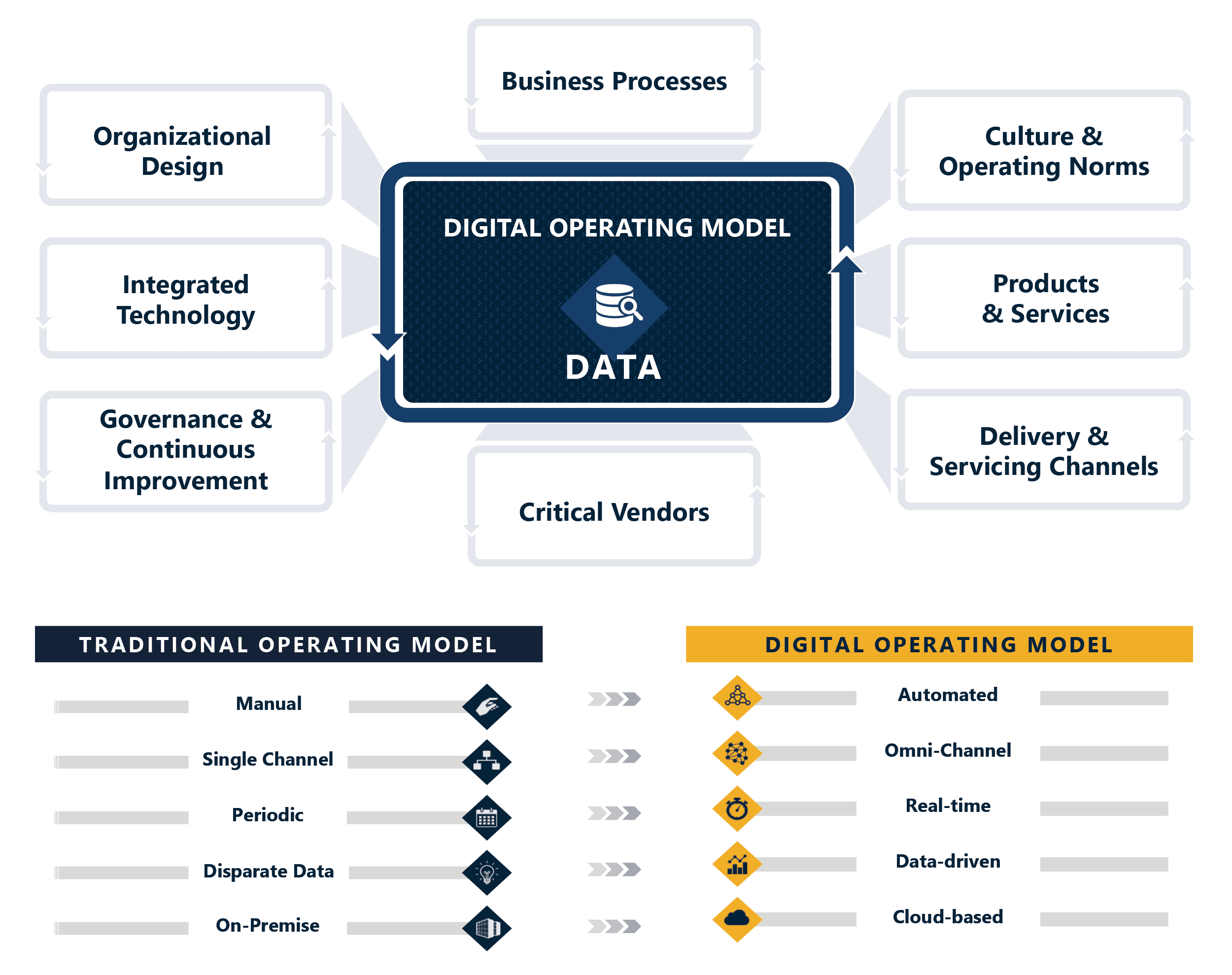

Data lives at the core of a digital op model—flowing throughout the value chain so leaders can gain and use insight to improve operations, create a scalable digital foundation, better deploy human capital, enhance client experience, and accelerate growth.

To meet these demands—from both the inside and out—banks must not only lean into the technology that will power new digital experiences, but also create this new digitally forward operating environment to power the entire enterprise. This includes designing a future operating model that aligns effort with reward in the front office, powers operations through new technologies, and enables data-driven decision-making.

Take this digital operating model example: a world where data flows seamlessly throughout your organization, driving operational efficiencies, generating insights, and improving customer experiences. Automation and integration decreases costs, saves time, reduces errors, and makes better use of human capital. Personalized interactions and self-service options—on numerous digital channels—create new revenue opportunities and meet the growing expectations of today’s customers. Data-driven credit decision models trim lending cycle times, streamline underwriting, and increase system wide capacity.

For today’s banks, offerings like these are no longer just a nice-to-have. They’re critical, and they’re becoming a necessity. Even before the pandemic, more than half of millennials would switch banks simply for a better mobile app. And in the past two years, catalyzed by the growing demand for more customized and efficient digital banking experiences, 1 in 5 adults have switched their primary bank.

A piecemeal approach won’t suffice. Banks must lay the foundation with a digital operating model, where data lives at the epicenter—and where, after a customer provides their information once, that data flows throughout the value chain, driving internal bank decision-making, delivering products and services to customers, and accelerating growth.

We’ve seen it happen. Banks that successfully adopt and scale a digital operating model see 30-40% capacity growth, 10-15% in annual cost savings, and their choice of degree for 20-25% market reinvestment.

Before diving into the specifics of a digital operating model, let’s take a step back and understand the base components of a general bank operating model.

This operating model is comprised of components that, when aggregated, deliver value to a bank’s customers and stakeholders while enabling future growth and scalability:

Overlaid atop this operating model is the organizational belief of “being digital.”

Being digital is more than taking individual actions when it comes to digital capabilities. It’s a way of doing business. It requires a mindset shift across every facet of an organization to move faster, to rely on data, and to put the customer at the center of every decision.

With this context, we arrive at the question: what is a digital operating model?

Though it represents the core of any bank’s digital operating model, procuring high-quality, real-time data often presents obstacles on numerous fronts. For instance, many banks often:

To help develop a digital operating model and address these issues, we’ve identified four critical components that create significant impact and unlock maximum value:

Business processes are ripe for investment across financial institutions, with process prioritizations driving revenue growth and increased productivity without growing headcount. Levers to address when considering transformative change through process enhancements include: reducing manual processes via Robotic Process Automation (RPA), increasing efficiencies via implementation of self-service capabilities, and improving resource utilization via capacity-management tools.

Integrate data, digital tools, and technology to enable users to enter data one time and have that data readily available to support all downstream processes. There are numerous opportunities across the product and customer lifecycles to streamline integrations in this manner, be it a front-end self-service portal or a fully integrated CRM and LOS platform—all leading to a centralized data warehouse.

Organizational design addresses re-alignment and optimization of responsibilities across roles while prioritizing employee performance, experience, and efficiency. The most efficient organizations prioritize upskilling key resources while aligning them to value-add activities.

Governance and continuous improvement. Advanced analytical maturity gained from a digital operating model enables banks to glean holistic insights into operations and drive organizational change. The transformative journey, however, doesn’t stop once an organization becomes digitally enabled and operationally efficient. It continues by utilizing organization change management and operational insights to continually upskill key resources, while streamlining processes from analytical discovery via ongoing monitoring.

Building off these components, we recommend utilizing the following self-assessment to gauge your readiness for a digital operating model:

In an increasingly competitive banking market, banks can’t afford to sit back and wait. By adopting a digital operating model, organizations will see opportunities to scale, increase revenue, reduce long-term costs, and lay the foundation for success in the digital age.